Understanding Your EPF: Saving for the Future

The EPF, or Employee Provident Fund, plays a vital role in securing your financial future in Malaysia. It's a savings scheme where both you and your employer contribute a portion of your salary. This accumulated amount is then available to you upon retirement, helping you maintain a comfortable lifestyle after your working years.

What are the benefits of the EPF?

- Retirement Savings: The EPF provides a nest egg for your golden years.

- Compound Interest: The EPF earns interest on your contributions, which further grows your savings over time.

- Tax Benefits: Both yours and your employer's contributions are generally tax-deductible.

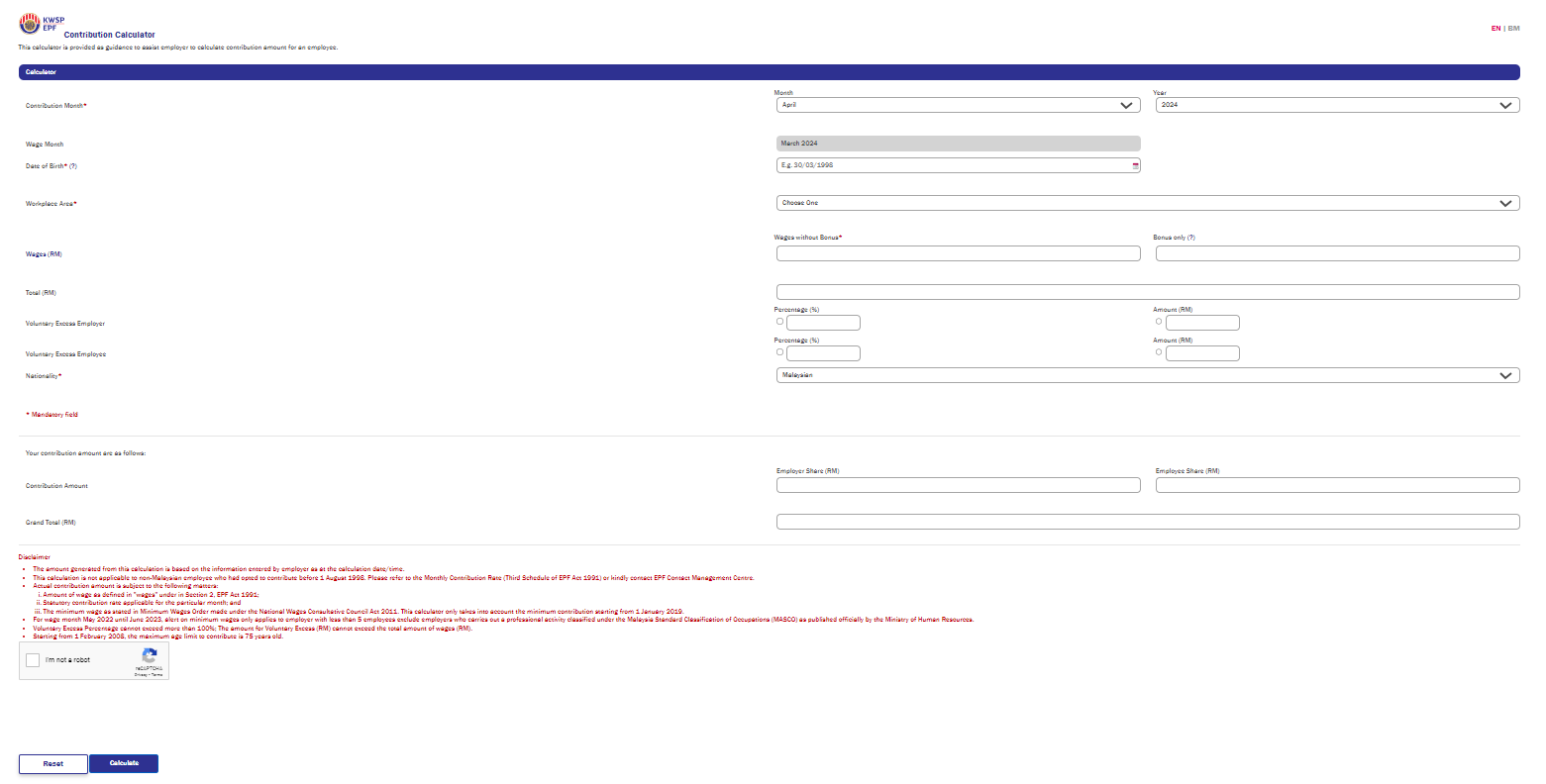

How is the EPF calculated?

The calculation is quite straightforward. Both you and your employer contribute a specific percentage of your basic salary (not including allowances) towards your EPF account. The current contribution rate for employees (as of April 2024) is 12% of your basic salary.

Here's a breakdown of employer contributions:

- Minimum 12% of your basic salary (for salaries above RM5,000)

- Minimum 13% of your basic salary (for salaries RM5,000 and below)

Important to note: There might be a maximum limit on the amount contributed, depending on regulations.

Let's look at an example:

Imagine your basic salary is RM4,000 per month. In this case:

- Your monthly EPF contribution: RM4,000 x 12% = RM480

- Employer's minimum contribution (assuming salary above RM5,000): RM4,000 x 12% = RM480

The total monthly contribution towards your EPF would be RM480 (yours) + RM480 (employer's) = RM960.

How can I access my EPF information online?

The good news is you can easily manage your EPF account online through the KWSP (Employees Provident Fund Board) website: KWSP website: https://www.kwsp.gov.my/en/. By registering for an online account, you can:

- View your EPF balance and contribution history.

- Update your personal details.

- Submit withdrawal applications (subject to eligibility).

Read more about EPF here: https://blog.kakitangan.com/epf-contribution-malaysia/

Learn directly from us during our monthly community series here: https://www.kakitangan.com/company/events