Statutory Changes for MTD 2021

Below is the summary of pre-announcement on statutory changes related to MTD 2021 in accordance to Budget 2021.

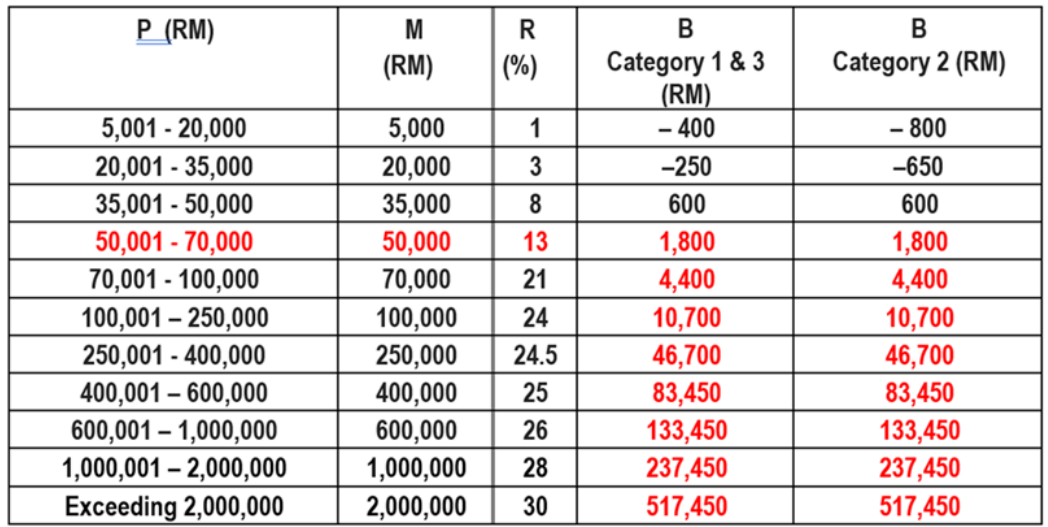

Tax rates changes

Starting from 2021, for tax residents who fall under chargeable income band from RM50,0001 to RM70,0000, tax rates to be reduced by 1%, from 14% to 13% as seen below chart.

Tax relief

Starting from 2021,

1. an additional tax relief limit for disable spouse to be increased from Rm3,5000 to RM5000.

2. an income tax relief for medical treatment, special needs and carer expenses for parents to be increased to up to RM8,000.

3. an income tax relief on medical expenses for serious diseases and fertility treatment for taxpayer and spouse to be increased to up to RM8,000, and complete medical examination expenses for self, spouse or child to up to RM1,000.

4. an additional tax relief on medical expenses further expanded to include vaccination expenses for tax payer, spouse and child up to up to RM1000.

5. an income tax relief for lifestyle to be included also on subscription for electronic newspapers.

6. an additional tax relief limited to RM500 on purchase of sports equipment, rental/entry fees for sports facilities and registration feeds in sports and competition for self, spouse and child.

7. an income tax relief on child care centres and kindergartens to be increased to RM3000.

8. an income tax relief on domestic tourism expenditure up to RM1,000 that made between 1st March to 31st December 2021, provided that the premises are registered under Commissioner of Tourism Malaysia and entrance fees to tourist attraction center.

9. an expansion of tax relief on education fees (self) to be expanded and covered courses of study undertaken for the purpose of up-skilling or self-enhancement, provided that the courses have to be conducted by a body recognized by the Director General Skills Development, under the National Skills Development Act 2006. Amount limited to Rm1,000 for each year and this amount to be part the existing tax relief of RM7,000.

10. an extension of tax relief on net deposit into SSPN (Skim Simpanaan Pendidikan Nasional) for another 2 years up to 2022.

11. an extension of tax relief on contribution to private retirement scheme and deferred annuity for another 4 years up to 2025.

12. an extension of tax incentive for returning experts for another 3 years that falls between 1st January 2021 to 31st December 2023, with revision of

a) Flat rate of 15% for a period of 5 consecutive years of assessment; and

b) Exemption on import duty and exercise duty for purchase of a CBU vehicles or excise duty exemption for the purchase of a CKD vehicle, subject to the total duty exemption limited up to RM100,000.

Note: The official announcement will be released after the amendment of Income Tax Act has been gazetted.